Qualitative Stories of Everyday Americans Navigating Today’s Economy

Behind every data point is a story. In Through Their Eyes: America’s Financial Reality, part of the SSRS Economic Attitudes Tracker, we hear directly from Americans navigating the realities of today’s economy — rising costs, shifting priorities, and the ongoing pursuit of stability.

To bring the data to life, we conducted in-depth follow-up interviews with respondents from Wave 4 of the Economic Attitudes Tracker using our SSRS Opinion Panel Qualibus. Their stories reveal what numbers alone cannot: the human side of economic shift — the resilience, worry, and hope shaping how Americans experience financial life today.

Here are Five of their Stories

Names, images, and identifying details have been changed to protect respondents’ privacy. Click the titles on the left to view each story.

Mary’s Story: Doing Everything Right, but Still Falling Behind

For most of her life, Mary has felt financially steady. She works full-time as a preschool teacher, her husband is retired, and until recently, her two adult children were working and self-sufficient. But in the past few months, everything has changed.

Her son lost his job of 18 years when his company laid off 30 people. Now he’s applying to “ten jobs a day” with no luck, while trying to make mortgage payments on a home he bought just last year. Her daughter was laid off from a freight company that closed its doors, leaving Mary to cover her car payment, phone bill, and even pet medications.

“I used to feel okay, but now I see what other people have been feeling. I’m helping my kids, and it’s getting tighter for us.” – Mary, 63, Florida

To make ends meet, Mary is cutting back on family traditions—hosting smaller holiday gatherings and asking relatives to bring dishes. The situation has left her anxious about the broader economy and the government shutdown. What once felt like a stable middle-class life now feels fragile.

“We’re not starving, but its’ getting tighter. Something has to give.” – Mary, 63, Florida

< Click the Next Title on the Left to Read Another Story

George’s Story: Working Hard, But Still Stuck

After years of scraping by, George finally felt like things were turning around. He landed a higher-paying job and started cutting back on expenses — progress that should have brought him some breathing room. But even with a raise, he says the math still doesn’t add up.

“Prices keep going up. Gas, household stuff – everything. And when stores close, the ones that stay open just jack the prices up. So yeah, I got a better job, but I still can’t get ahead.” – George, 46, Tennessee

He earns about $21 an hour building cooling towers and circuit breaker boxes — work he’s proud of, but a wage that doesn’t match the skill or effort it requires.

“$20 an hour used to mean something. Now it’s basically minimum wage. You can only do the bare necessities.” – George, 46, Tennessee

George dreams of buying a house instead of renting and wants to invest in stocks like Nike or Amazon, but says those goals feel out of reach. For now, he’s focused on stability and caring for his five children.

What worries him most isn’t just his own situation, but what he sees happening around him. He’s watched family members come out of retirement because they can’t afford to stay home — like his aunt, a lifelong nurse, and an 84-year-old former coworker who had to return to work despite poor health.

“When you retire, you’re supposed to be comfortable. You shouldn’t have to go back to work just to survive.” – George, 46, Tennessee

For George, financial security isn’t about wealth — it’s about finally being able to save, breathe, and stop living paycheck to paycheck.

“To America, I’m probably not poor. But to me, I am – because I’m just getting by.” – George, 46, Tennessee

< Click the Next Title on the Left to Read Another Story

Madison’s Story: Working Hard to Give Her Kids a Better Life

Madison has always been diligent about managing her finances, but the past year has left her feeling overwhelmed. Despite working constantly and picking up extra hours whenever possible, unexpected expenses keep piling up. She’s meticulous about paying bills on time, yet it feels impossible to get ahead.

“No matter how much I try to move a little bit forward, something else keeps adding to it. It just feels really overwhelming.” – Madison, 40, New York

A major setback came after surgery, when Madison didn’t receive the support she expected from her job or government services. She relied on credit cards to stay afloat, and the recovery period stretched her finances thin.

“Basically, the only thing I was really not having to worry for was food…but everything else… everything else got hard.” – Madison, 40, New York

Her financial stress also affects her family life. She wants to give her daughter the typical experiences of a teenager — preparing for her 16th birthday, celebrating Christmas — but resources are tight.

“It’s just really hard, trying to make do with what you got… it’s not the way I guess they would like it to be. That really bothers me. But so far, I guess I could say that I’ve raised them well, so they do understand, but that doesn’t make me happy.” – Madison, 40, New York

For Madison, financial security means simple stability — being able to meet needs without the constant anxiety of what might go wrong next.

“If my daughter needed something for school last minute, I wouldn’t have to figure out, ‘well, where am I getting this from?’ That’s what financial stability looks like for me.” – Madison, 40, New York

Reflecting on her younger years, Madison wishes she had been able to save more.

“If I could go back, I would have just saved, saved, saved. Even a little stash would have been so helpful right now.” – Madison, 40, New York

Despite the challenges, she continues to work hard, juggle responsibilities, and teach her children the value of managing money wisely—but the road to feeling financially secure remains slow and difficult.

< Click the Next Title on the Left to Read Another Story

John’s Story: A Lifetime of Work, and Still Not Secure

At 65, John rates his financial comfort a “six out of ten.” He and his wife have some savings, but with her nearing retirement and the rising cost of living, he worries about what comes next.

“We have some savings and my wife’s about to retire, but with the cost of rent and everything else, there’s always concern we could end up in a bind.” – John, 65, California

After losing a small income caring for his late mother, John has found it harder to make ends meet. His Social Security isn’t enough, and his handyman work comes and goes. At his age, finding steady employment has proven difficult.

“I’d work anywhere – Home Depot, Walmart – but my age and time out of the workforce make it tough to get an opportunity.” – John, 65, California

He and his wife have spent their lives working hard and helping their family when they can, but they’ve never had the chance to truly feel secure. For John, financial security would mean something simple and profound: owning a home and having enough savings to stop worrying. But these goals feel increasingly out of reach.

< Click the Next Title on the Left to Read Another Story

Alex’s Story: Keeping Afloat, One Bill at a Time

Alex has always tried to keep the household running smoothly, but rising costs and limited income have made it feel like treading water. Rent goes up every year, groceries are more expensive, and the family’s food stamps have been reduced. Despite careful budgeting, it seems like there’s never enough to get ahead.

“Everything keeps going up…it just seems like we can’t get ahead.” – Alex, 46, Nevada

Even though Alex and their partner pay all the bills and keep the lights on, they worry constantly about whether they can make it through the month. Air conditioning in Las Vegas is a necessity, but it comes with shocking electricity bills that add to the strain.

“It’s always a worry about whether we can pay all the rent when it’s due… making sure that we have enough to pay all the bills and have enough left over for food.” – Alex, 46, Nevada

To make ends meet, Alex’s partner has returned to donating plasma for extra income, a strategy they learned about years ago from a friend.

Alex dreams of small comforts for the family that feel out of reach—like taking the kids to a movie or enjoying a night out bowling.

“My wish is for all of our bills paid without late payments, without worry…and being able to, like I said, go to a movie once a month.” – Alex, 46, Nevada

Reflecting on the past, Alex wishes they had saved more. Even a modest cushion of $1,500 for unexpected emergencies, like car repairs or small household costs, would bring a sense of relief and security.

“Try to save. Try to save. Make a little nest egg.” – Alex, 46, Nevada

Mary’s Story: Doing Everything Right, but Still Falling Behind

For most of her life, Mary has felt financially steady. She works full-time as a preschool teacher, her husband is retired, and until recently, her two adult children were working and self-sufficient. But in the past few months, everything has changed.

Her son lost his job of 18 years when his company laid off 30 people. Now he’s applying to “ten jobs a day” with no luck, while trying to make mortgage payments on a home he bought just last year. Her daughter was laid off from a freight company that closed its doors, leaving Mary to cover her car payment, phone bill, and even pet medications.

“I used to feel okay, but now I see what other people have been feeling. I’m helping my kids, and it’s getting tighter for us.” – Mary, 63, Florida

To make ends meet, Mary is cutting back on family traditions—hosting smaller holiday gatherings and asking relatives to bring dishes. The situation has left her anxious about the broader economy and the government shutdown. What once felt like a stable middle-class life now feels fragile.

“We’re not starving, but its’ getting tighter. Something has to give.” – Mary, 63, Florida

< Click the Next Title on the Left to Read Another Story

George’s Story: Working Hard, But Still Stuck

After years of scraping by, George finally felt like things were turning around. He landed a higher-paying job and started cutting back on expenses — progress that should have brought him some breathing room. But even with a raise, he says the math still doesn’t add up.

“Prices keep going up. Gas, household stuff – everything. And when stores close, the ones that stay open just jack the prices up. So yeah, I got a better job, but I still can’t get ahead.” – George, 46, Tennessee

He earns about $21 an hour building cooling towers and circuit breaker boxes — work he’s proud of, but a wage that doesn’t match the skill or effort it requires.

“$20 an hour used to mean something. Now it’s basically minimum wage. You can only do the bare necessities.” – George, 46, Tennessee

George dreams of buying a house instead of renting and wants to invest in stocks like Nike or Amazon, but says those goals feel out of reach. For now, he’s focused on stability and caring for his five children.

What worries him most isn’t just his own situation, but what he sees happening around him. He’s watched family members come out of retirement because they can’t afford to stay home — like his aunt, a lifelong nurse, and an 84-year-old former coworker who had to return to work despite poor health.

“When you retire, you’re supposed to be comfortable. You shouldn’t have to go back to work just to survive.” – George, 46, Tennessee

For George, financial security isn’t about wealth — it’s about finally being able to save, breathe, and stop living paycheck to paycheck.

“To America, I’m probably not poor. But to me, I am – because I’m just getting by.” – George, 46, Tennessee

< Click the Next Title on the Left to Read Another Story

Madison’s Story: Working Hard to Give Her Kids a Better Life

Madison has always been diligent about managing her finances, but the past year has left her feeling overwhelmed. Despite working constantly and picking up extra hours whenever possible, unexpected expenses keep piling up. She’s meticulous about paying bills on time, yet it feels impossible to get ahead.

“No matter how much I try to move a little bit forward, something else keeps adding to it. It just feels really overwhelming.” – Madison, 40, New York

A major setback came after surgery, when Madison didn’t receive the support she expected from her job or government services. She relied on credit cards to stay afloat, and the recovery period stretched her finances thin.

“Basically, the only thing I was really not having to worry for was food…but everything else… everything else got hard.” – Madison, 40, New York

Her financial stress also affects her family life. She wants to give her daughter the typical experiences of a teenager — preparing for her 16th birthday, celebrating Christmas — but resources are tight.

“It’s just really hard, trying to make do with what you got… it’s not the way I guess they would like it to be. That really bothers me. But so far, I guess I could say that I’ve raised them well, so they do understand, but that doesn’t make me happy.” – Madison, 40, New York

For Madison, financial security means simple stability — being able to meet needs without the constant anxiety of what might go wrong next.

“If my daughter needed something for school last minute, I wouldn’t have to figure out, ‘well, where am I getting this from?’ That’s what financial stability looks like for me.” – Madison, 40, New York

Reflecting on her younger years, Madison wishes she had been able to save more.

“If I could go back, I would have just saved, saved, saved. Even a little stash would have been so helpful right now.” – Madison, 40, New York

Despite the challenges, she continues to work hard, juggle responsibilities, and teach her children the value of managing money wisely—but the road to feeling financially secure remains slow and difficult.

< Click the Next Title on the Left to Read Another Story

John’s Story: A Lifetime of Work, and Still Not Secure

At 65, John rates his financial comfort a “six out of ten.” He and his wife have some savings, but with her nearing retirement and the rising cost of living, he worries about what comes next.

“We have some savings and my wife’s about to retire, but with the cost of rent and everything else, there’s always concern we could end up in a bind.” – John, 65, California

After losing a small income caring for his late mother, John has found it harder to make ends meet. His Social Security isn’t enough, and his handyman work comes and goes. At his age, finding steady employment has proven difficult.

“I’d work anywhere – Home Depot, Walmart – but my age and time out of the workforce make it tough to get an opportunity.” – John, 65, California

He and his wife have spent their lives working hard and helping their family when they can, but they’ve never had the chance to truly feel secure. For John, financial security would mean something simple and profound: owning a home and having enough savings to stop worrying. But these goals feel increasingly out of reach.

< Click the Next Title on the Left to Read Another Story

Alex’s Story: Keeping Afloat, One Bill at a Time

Alex has always tried to keep the household running smoothly, but rising costs and limited income have made it feel like treading water. Rent goes up every year, groceries are more expensive, and the family’s food stamps have been reduced. Despite careful budgeting, it seems like there’s never enough to get ahead.

“Everything keeps going up…it just seems like we can’t get ahead.” – Alex, 46, Nevada

Even though Alex and their partner pay all the bills and keep the lights on, they worry constantly about whether they can make it through the month. Air conditioning in Las Vegas is a necessity, but it comes with shocking electricity bills that add to the strain.

“It’s always a worry about whether we can pay all the rent when it’s due… making sure that we have enough to pay all the bills and have enough left over for food.” – Alex, 46, Nevada

To make ends meet, Alex’s partner has returned to donating plasma for extra income, a strategy they learned about years ago from a friend.

Alex dreams of small comforts for the family that feel out of reach—like taking the kids to a movie or enjoying a night out bowling.

“My wish is for all of our bills paid without late payments, without worry…and being able to, like I said, go to a movie once a month.” – Alex, 46, Nevada

Reflecting on the past, Alex wishes they had saved more. Even a modest cushion of $1,500 for unexpected emergencies, like car repairs or small household costs, would bring a sense of relief and security.

“Try to save. Try to save. Make a little nest egg.” – Alex, 46, Nevada

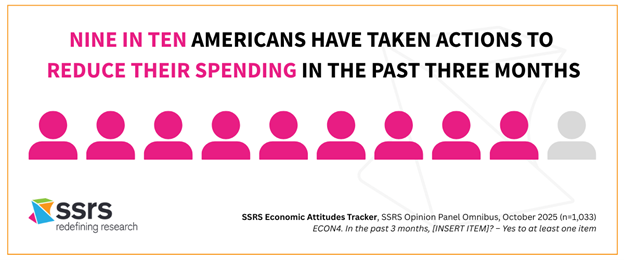

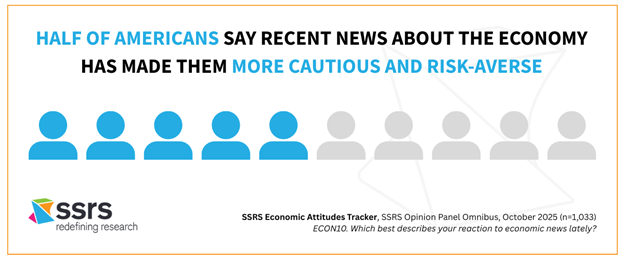

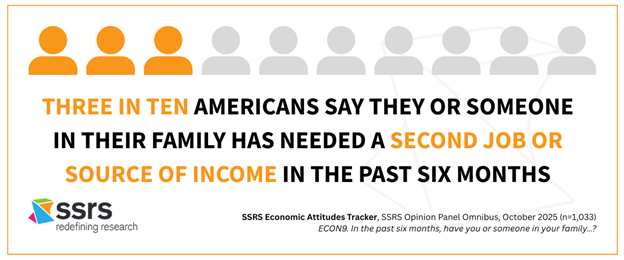

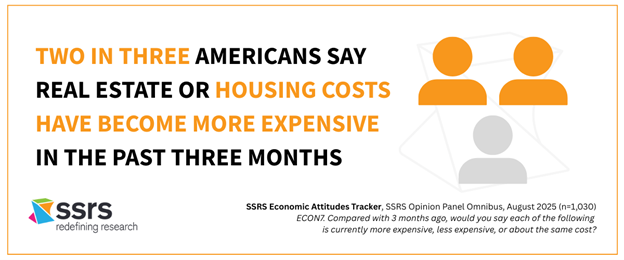

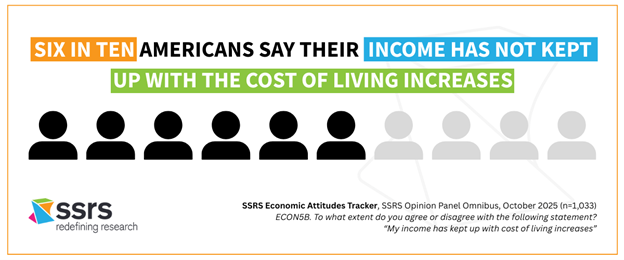

The Economic Attitudes Tracker is conducted by SSRS on its Opinion Panel Omnibus platform. The SSRS Opinion Panel Omnibus is a national, twice-per-month, probability-based survey.

Join Our Economic Trends Mailing List

Economic Attitudes Tracker waves include:

March 21 – March 24, 2025 among a sample of 1,031 panelists. The survey was conducted via web (n=1,001) and telephone (n=30) and administered in English (n=1,005) and Spanish (n=26). The margin of error for total respondents is +/-3.8 percentage points at the 95% confidence level. The design effect is 1.54.

June 6 – June 10, 2025 among a sample of 1,029 respondents. The survey was conducted via web (n=999) and telephone (n=30) and administered in English (n=1,004) and Spanish (n=25). The margin of error for total respondents is +/-3.5 percentage points at the 95% confidence level. The design effect is 1.29.

August 1 – August 4, 2025 among a sample of 1,030 respondents. The survey was conducted via web (n=1,000) and telephone (n=30) and administered in English (n=1,004) and Spanish (n=26). The margin of error for total respondents is +/-3.5 percentage points at the 95% confidence level. The total sample design effect for this survey is 1.31.

October 16 – October 19, 2025 among a sample of 1,033 respondents. The survey was conducted via web (n=1,003) and telephone (n=30) and administered in English (n=1,007) and Spanish (n=26). The margin of error for total respondents is +/-3.5 percentage points at the 95% confidence level. The total sample design effect for this survey is 1.34. SSRS selected six respondents who had expressed in the survey that they were experiencing some form of financial challenge to take part in a qualitative follow-up interview. Using our SSRS Opinion Panel Qualibus methodology, we invited them to participate in a 30-minute Zoom interview with a SSRS researcher between October 28-30, 2025.

All SSRS Opinion Panel Omnibus data are weighted to represent the target population of U.S. adults ages 18 or older.

The SSRS Opinion Panel Omnibus is conducted on the SSRS Opinion Panel. SSRS Opinion Panel members are recruited randomly based primarily on nationally representative ABS (Address Based Sample) design (including Hawaii and Alaska). ABS respondents are randomly sampled by Marketing Systems Group (MSG) through the U.S. Postal Service’s Computerized Delivery Sequence File (CDS), a regularly updated listing of all known addresses in the U.S. For the SSRS Opinion Panel, known business addresses are excluded from the sample frame. Additional panelists are recruited via random digit dial (RDD) telephone sample of cell phone numbers connected to a prepaid cell phone. This sample is selected by MSG from the cell phone RDD frame using a flag that identifies prepaid numbers. Prepaid cell numbers are associated with cell phones that are “pay as you go” and do not require a contract.

The SSRS Opinion Panel is a multi-mode panel (web and phone). Most panelists take self-administered web surveys; however, the option to take surveys conducted by a live telephone interviewer is available to those who do not use the internet as well as those who use the internet but are reluctant to take surveys online.

Strategic Questions Deserve Strategic Answers

At SSRS, we help organizations answer their most pressing questions with clarity, confidence, and strategic insight. Whether you’re responding to emerging challenges, planning for the future, or fine-tuning your messaging, we’re here to help you see clearly, act confidently, and lead with insight. If this topic resonates with you—or sparks new questions—we’d love to connect.